Short Sale vs Foreclosure

Short Sale vs Foreclosure: Which Option Is Right for Your LA Home? When homeowners in Los Angeles face financial hardship, two paths often emerge: s...

Short Sale vs Foreclosure: Which Option Is Right for Your LA Home?

When homeowners in Los Angeles face financial hardship, two paths often emerge: short sales and foreclosure. Having worked with distressed properties throughout LA County, Orange County, and the surrounding areas, I've guided countless families through both processes. The choice between these options can significantly impact your financial future, credit score, and ability to purchase another home.

Let me walk you through the key differences and help you understand which path might be right for your situation.

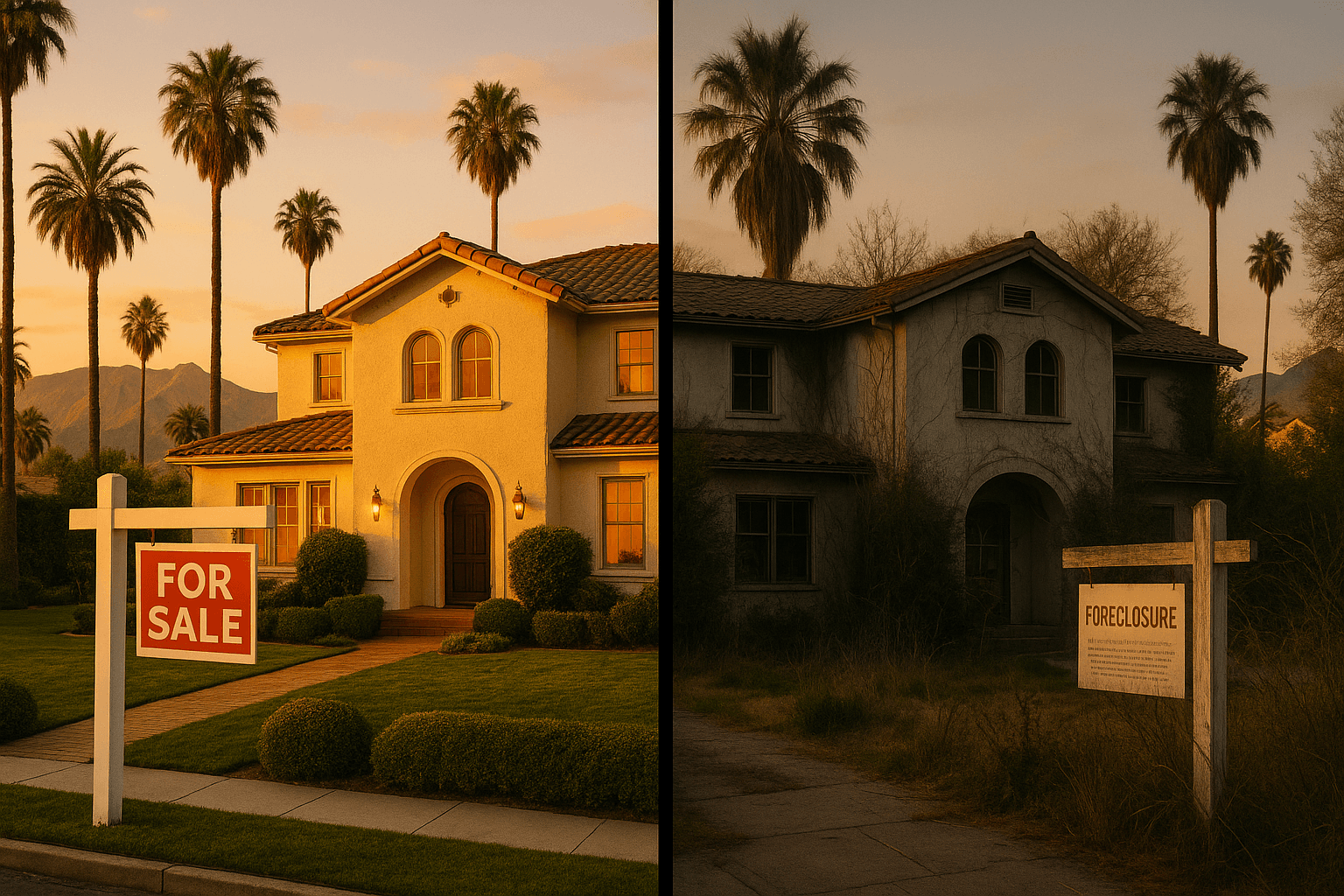

What Is a Short Sale?

A short sale occurs when you sell your home for less than what you owe on your mortgage, with your lender's approval. Essentially, the lender agrees to accept less than the full loan balance to avoid the lengthy and costly foreclosure process.

In neighborhoods like Beverly Hills, Santa Monica, or even more affordable areas like Van Nuys or Pomona, I've seen homeowners successfully navigate short sales when their property values dropped below their mortgage balances or when life circumstances made payments impossible.

Short Sale Process Timeline

The short sale process typically takes 3-6 months from listing to closing, though it can extend longer depending on your lender's response time. Here's what you can expect:

- Initial consultation and hardship documentation

- Listing the property with a qualified agent

- Negotiating offers with potential buyers

- Submitting the short sale package to your lender

- Waiting for lender approval (often the longest part)

- Closing once approved

What Is Foreclosure?

Foreclosure is a legal process where your lender takes possession of your property due to missed mortgage payments. In California, most foreclosures are non-judicial, meaning they don't require court intervention. The process moves relatively quickly once it begins.

From my experience working with homeowners from Riverside to Ventura County, foreclosure often feels like losing control of your situation entirely. The lender sets the timeline, and your input becomes minimal once the process starts.

Foreclosure Process Timeline

California's foreclosure process typically takes 4-7 months:

- Notice of Default (NOD) filed after 90+ days of missed payments

- 3-month reinstatement period

- Notice of Trustee Sale posted and published

- 21-day notice before the actual sale

- Trustee sale (auction)

Credit Score Impact: The Numbers Matter

One of the most significant differences between these options lies in their impact on your credit score.

Short Sale Credit Impact

A short sale typically drops your credit score by 50-150 points. While this seems substantial, it's generally less damaging than foreclosure. Most importantly, you may be eligible for a new mortgage in as little as 2-4 years, depending on your lender and circumstances.

Foreclosure Credit Impact

Foreclosure can devastate your credit score, often dropping it by 200-300 points. The recovery period is typically longer, with most conventional loans requiring a 7-year waiting period before you can qualify for another mortgage.

Financial Consequences Beyond Credit

Short Sale Financial Impact

With a short sale, you maintain more control over the process and timeline. In California, lenders cannot pursue deficiency judgments on purchase money first mortgages, which provides some protection. However, second mortgages or refinanced loans might still create liability, so consulting with a qualified attorney is essential.

Foreclosure Financial Impact

Foreclosure often means losing any equity in your home and facing potential deficiency judgments on certain types of loans. Additionally, you'll need to vacate the property, often with little control over timing.

Which Option Provides More Control?

Having worked with families throughout Los Angeles—from the Hollywood Hills to Long Beach—I've observed that short sales offer significantly more control over your situation.

Short Sale Control Factors

- You choose when to list

- You participate in buyer selection

- You negotiate terms with your lender

- You maintain possession longer

- You avoid the public nature of foreclosure auctions

Foreclosure Control Factors

Once foreclosure proceedings begin, you have limited options:

- The lender controls the timeline

- You must vacate by a specific date

- No input on the new owner

- Public record of the foreclosure follows you

Tax Implications to Consider

Both options can have tax consequences that require professional guidance. The Mortgage Forgiveness Debt Relief Act provided some protections, but tax laws change frequently. I always recommend consulting with a qualified tax professional to understand your specific situation.

When Short Sale Makes Sense

Based on my experience helping homeowners from San Bernardino to Ventura County, short sales often work best when:

- You're current on payments but facing hardship

- Your home's value is less than what you owe

- You have time to navigate the process (3-6 months minimum)

- You want to minimize credit damage

- You're experiencing divorce, job loss, medical issues, or other qualifying hardships

When Foreclosure Might Be Inevitable

Sometimes foreclosure becomes the only option:

- You're already months behind on payments

- Your lender won't approve a short sale

- You cannot qualify for loan modification

- You need to move quickly due to circumstances

Working with the Right Professional Team

Whether you choose a short sale or face foreclosure, having experienced professionals makes a tremendous difference. As someone certified in Short Sales and Foreclosures, I've seen how proper representation can save homeowners thousands of dollars and months of stress.

Your team should include:

- A real estate agent certified in distressed properties

- An attorney familiar with California foreclosure law

- A tax professional who understands debt forgiveness

- Your lender's loss mitigation department

Moving Forward: Your Next Steps

If you're facing this difficult decision in LA County, Orange County, Riverside, San Bernardino, or Ventura County, you don't have to navigate it alone. Every situation is unique, and what works for a homeowner in Manhattan Beach might not be the right solution for someone in Lancaster or Thousand Oaks.

The most important step is acting quickly. Whether you're just starting to struggle with payments or you've already received a Notice of Default, earlier intervention provides more options.

Don't let fear or embarrassment prevent you from exploring your options. I've helped families in every type of neighborhood and situation find solutions that protect their futures.

Ready to discuss your specific situation? Visit homenest.house to learn more about your options, or call me directly at 323-472-7059. Let's work together to find the path forward that makes the most sense for your family's future.

Have a question about your home?

Suzanna Saharyan and the HomeNest team help homeowners across Southern California make confident moves. Get a free home value estimate or talk to a real human — no spam, no pressure.